RSS Feed

RSS Feed by Calculated Risk on 12/09/2006 07:25:00 PM

Saturday, December 09, 2006

Northern Trust Economic Outlook

Congratulations to Paul Kasriel, the recipient of the 2006 Lawrence R. Klein Award for Blue Chip Forecasting Accuracy:

"Kasriel [was] honored for having the most accurate economic forecast among the Blue Chip survey participants for the years 2002 through 2005."From the Northern Trust December Economic Outlook:

We continue to expect sub-2% annualized real GDP growth in the final quarter of this year and have revised down our first-quarter 2007 forecast to 1.8% from 2.0% -- not much more than a rounding error. In addition to the fifth consecutive quarterly decline in real residential investment expenditures, we expect a considerable deceleration in the growth of real business expenditures for capital equipment and software in the fourth quarter, based on the weak October shipments data for nondefense capital goods excluding aircraft. ...

Based on the excesses of the past real estate boom, the considerable supply overhang and the typical peak-to-trough behavior of residential investment expenditures, we continue to expect that the trough of the housing recession is not near at hand....

Click on graph for larger image.

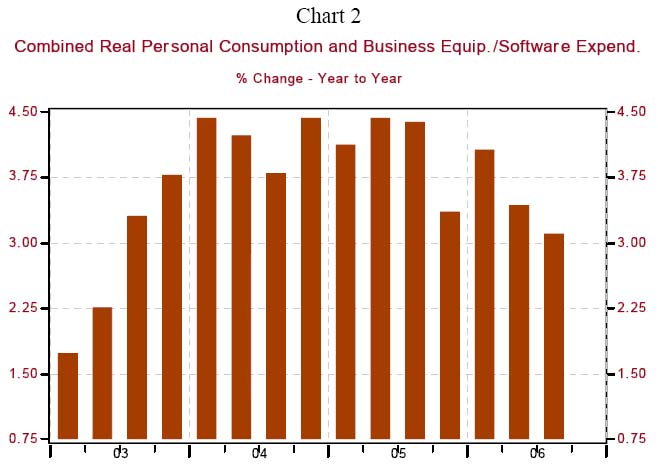

Click on graph for larger image.We continue to hear that the weakness in housing has not spread to other parts of the economy. To that we say “Not so” and “You ain’t seen nothin’ yet.” As Chart 2 shows, the year-over-year growth in combined real personal consumption and business equipment/software expenditures, at 3.1% in the third quarter, is the slowest since the second quarter 2003 and is down 130 basis points from its year-ago growth. That takes care of the “not so.”

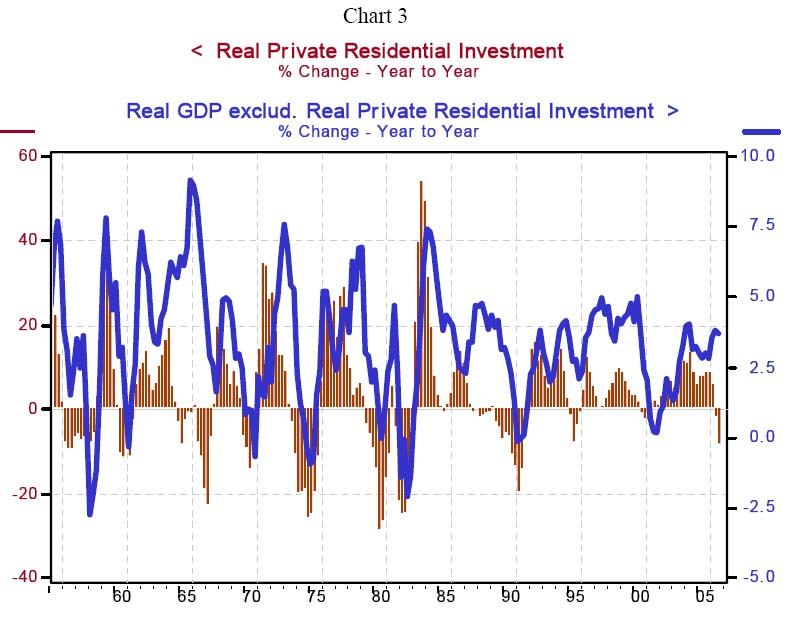

With regard to the “you-ain’t-seen-nothin’-yet” argument, take a look at Chart 3. You don’t have to examine it closely to see that the year-over-year behavior of residential investment expenditures leads the behavior of the rest of the economy. If you did look closely, you would see that the lead time tends to be about two calendar quarters. This implies that even if the trough of the housing recession is at hand, the full ripple effects from the weak housing sector have yet to lap up on the shore of the rest of the economy. Moreover, if the housing-recession trough lies ahead, the wave action from this sector will continue through most of 2007.Currently Northern Trust is forecasting 1.6% real annualized GDP growth in Q4, and 1.8%, 2.0%, 2.4% and 3.0% for each successive quarter in 2007. This is a forecast for sluggish growth in 2007, without a recession, and is similar to the Anderson forecast.

Another reason we believe the recession in housing will have a lingering retarding effect on economic activity concerns its impact on the “home ATM”, i.e., mortgage equity withdrawal (MEW). With home prices either falling or advancing more slowly, depending on the price series used, it stands to reason that growth in homeowners’ equity would be slowing.... So, the home ATM is not refilling as rapidly as it has in recent years. The slower growth in home equity along with the higher level of mortgage and home equity loan interest rates is slowing MEW, an important source of funding for household spending in recent years.